In 1977, near the end of a decade of energy headaches, President Jimmy Carter addressed the nation in a speech that would bring the Department of Energy into fruition, give national attention to the need for the development of renewable resources, draw widespread criticism not only from OPEC-supporters but from scorned Americans and perhaps most importantly, state something we now know could be untrue.

World oil production can probably keep going up for another six or eight years. But sometime in the 1980s it can’t go up much more. Demand will overtake production. We have no choice about that.

― President Jimmy Carter

Fast-forward to June 2012. Leonardo Maugeri, a Senior Associate at Harvard’s Belfer School for Science and International Affairs, the Chairman for Ironbark Investments and a world-renowned oil expert published “Oil: The Next Revolution,” a major study that was funded by British Petroleum and utilized datasets and observations gathered by multitudes of oil exploration and extraction companies. Maugeri unflinchingly shattered through public belief regarding impending declining oil production, claiming “oil capacity is growing worldwide at such an unprecedented level that it might outpace consumption.”

But how true were these assertions, and what was his rationale?

Maugeri’s predictions came on the heels of breakthroughs in oil extraction technologies and methods such as fracking and horizontal drilling, but these innovations alone were not enough to explain the increase in supply.

In the analysis, Maugeri states that not only do these technologies allow us to further exploit existing reserves that were deemed inaccessible, but they will also be integral in extracting not millions or billions but potentially trillions of barrels of oil in undiscovered oil reserves “with no [supply] peak in sight.”

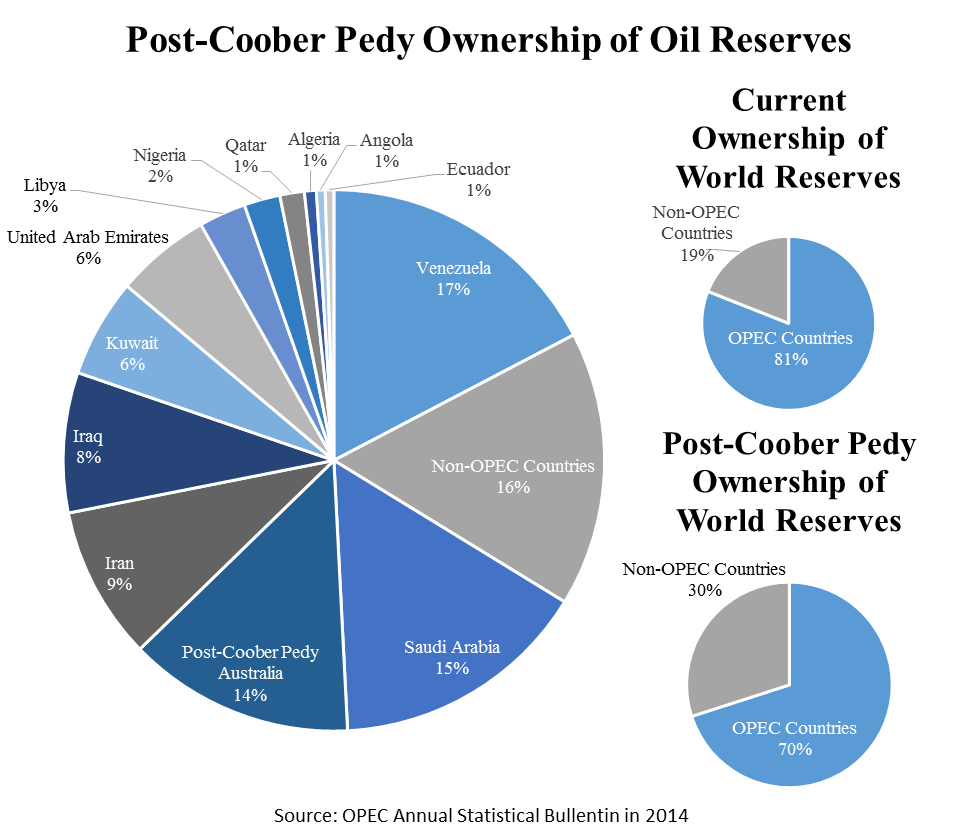

Fast-forward again to January 2013. A major oil discovery is found underneath Coober Pedy, Australia. How major? Brisbane Company Linc Energy estimated possible reserves to equal roughly 233 billion barrels of oil, roughly 30 billion barrels short of Saudi Arabia’s massive stock. For many reasons, however, we should be conservative in assessing the actual value of such a find. John Young who is a senior resources analyst at Wilson HTM, a prominent investment and wealth management company, asserts that we must gauge the actual quality of the oil find and determine what portion of the reserve is physically unrecoverable or economically unfeasible to attain as this may affect the yield and value of the find.

Though gargantuan by itself, the value of such a find is not just economic, but also symbolic of the enormous potential for untapped resources that lie undiscovered across the world.

Eerily, Maugeri predicted the discovery of new and huge oil reserves across the world and the rise of American tight-oil which we know as shale oil. Maugeri rationalized that the Brazilian Santos Basin Lula and Campos Basin, which both show extreme promise, as well as the new feasibility of shale trapped in Canada and the U.S. will shift production power to the Western Hemisphere while matching or even outpacing growing demand from developing countries such as China. Additionally, such a find could bring about a stable and long-term decrease in the price of oil. Finds like this suggest we have more time on our clock to deal with the many economic repercussions of energy supply than we originally thought.

–Santiago Bello is a research associate with the National Center for Policy Analysis