Evolving Energy Infrastructure — Energy Battles Looming at Home

The electrical utilities industry is one that has always been regarded by economists as unique, with its most defining aspect being competition. There is little to none. However, economists have always argued that this is only a rational byproduct of the infrastructure associated with transporting energy. A perfectly competitive market is saturated with companies, and with hundreds or even thousands of different energy companies, the power lines and facilities required to generate electricity would be astronomically inefficient. For this reason, infrastructure in this field has been widely shielded from the pressures brought by rival businesses and increasingly demanding customers.

The free market could be on the verge of changing these norms. It all begins with introducing an adversarial element to the electrical utilities sector.

Vivek Wadhwa, a fellow at the Rock Center for Corporate Governance at Stanford University and the director of research at Duke’s Center for Entrepreneurship and Research Commercialization begins the topic of evolving energy at its root: Many forms of energy are outdated or considered too dangerous. President Obama’s recent energy accords in India is an example of this, with Wadhwa stating,

This is hardly a victory for the United States or for India. It no longer makes sense for any country to install a technology that can create a catastrophe such as Chernobyl or Fukushima — especially when far better alternatives are available.

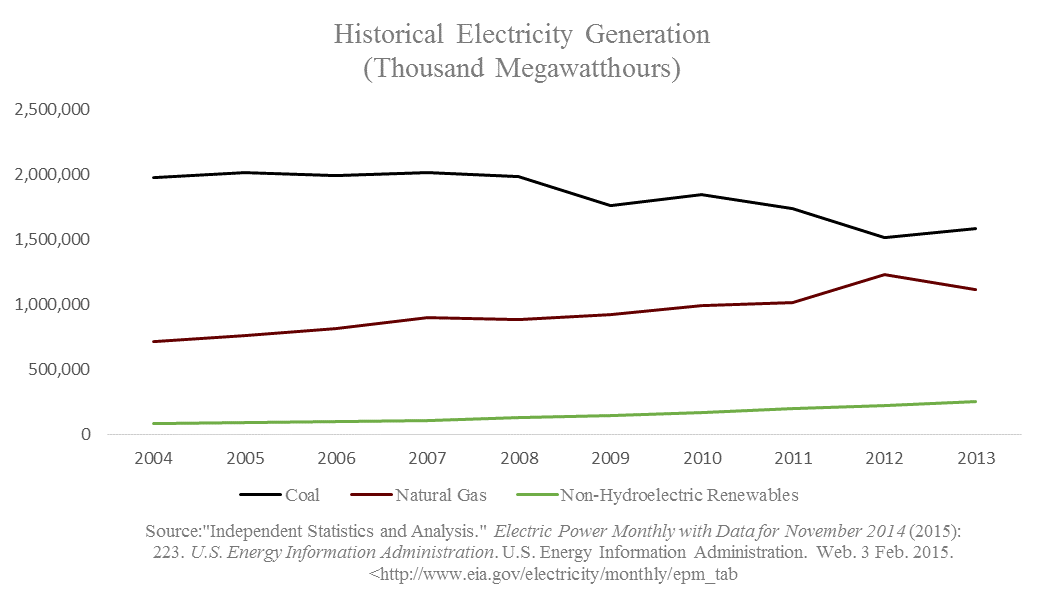

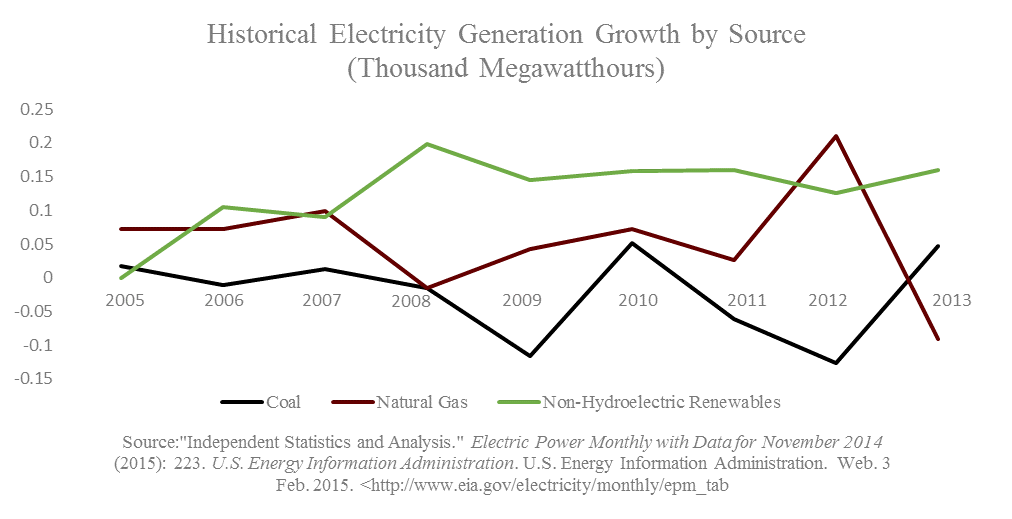

Furthermore, Wadhwa points out that nuclear facilities and growth in the nuclear energy sector has been stagnant compared to coal, natural gas and renewables, a claim largely supported by the Energy Information Administration’s statistics on U.S. energy consumption.

The president should not be prescribing medicine [to electrical consumption] that he would not take himself.

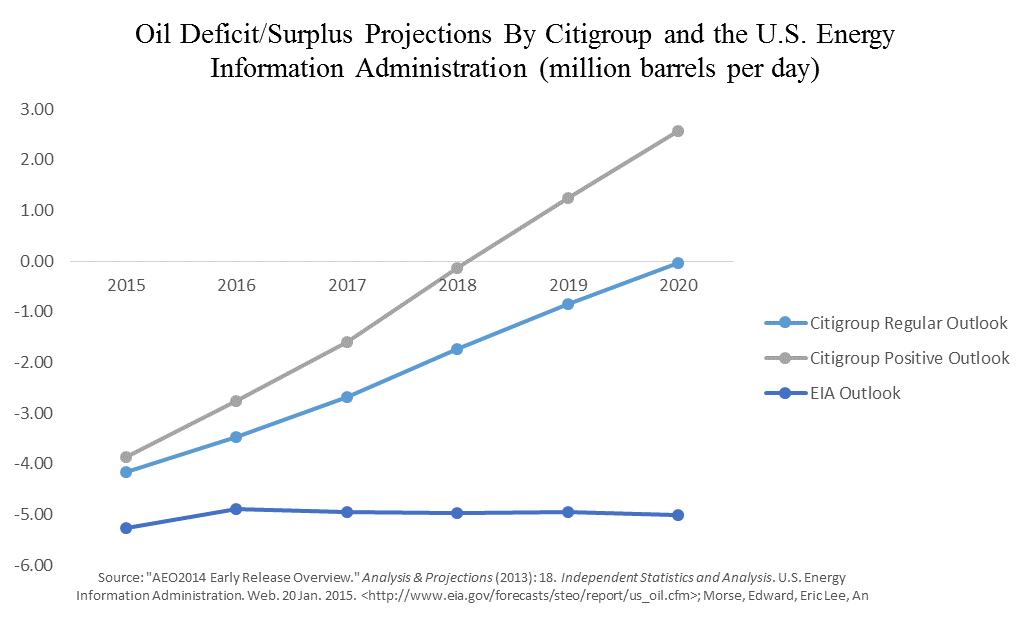

In a 2014 report, “Energy 2020: The Revolution Will Not Be Televised as Disruptors Multiply,” Citigroup claims that coal has suffered a serious double threat with the resurgence of natural gas during America’s shale revolution, and most surprisingly the projected ― not current ― falling costs of solar energy.

Indeed, natural gas and renewables such as solar are also the only two major methods of energy production which have consistently expanded at a positive rate for many years. Oil has historically been rarely used by electrical utility companies, and hydroelectric energy ― which does account for significant amounts of energy in the U.S. ― has largely been stagnant in meeting our rising demand for energy.

The growing popularity of renewables such as solar and wind has been a phenomenon that has been observed mainly in Europe. In a separate article, “The Coming Era of Unlimited ― and Free ― Clean Energy,” Wadhwa explains many countries in Europe have reached grid parity, a state in which installing electrical grids powered by wind and photovoltaics have matched energy prices from conventional electrical power plants. Were such a phenomenon to begin in the United States, it would be horrible news for coal, which is already hobbling along, largely due to the higher costs imposed by environmental regulations.

Solar and wind’s capacity for powering microgrids — grids which operate in the local vicinity in which their consumers reside — could also put pressure on the entire infrastructure that American energy needs have relied on for years. America’s energy infrastructure is also vastly outdated — with the best example of such being the Northeast’s chronically faltering electrical grid. The lack of innovation and improvement is mainly due to the lack of competition in the sector. Though solar and wind energy is still years away from being able to match domestic prices, advances in microgrid popularity which would be enabled by Citi’s projected foreign investment in the two energies could introduce choice to the energy sector, effectively lowering prices and helping America in its quest to be energy independent.