Toxic Assets, Financial Sector Projections and… Bubbles?

As many economically-informed Americans know, the Great Recession of 2007 was instigated largely by belligerent lending by some of the largest banks in the United States — specifically a crisis started by aspiring homeowners and banks, who both overestimated the future value of the home, and investors who largely misunderstood the financial instruments called derivatives, whose market value originated from those same home loans.

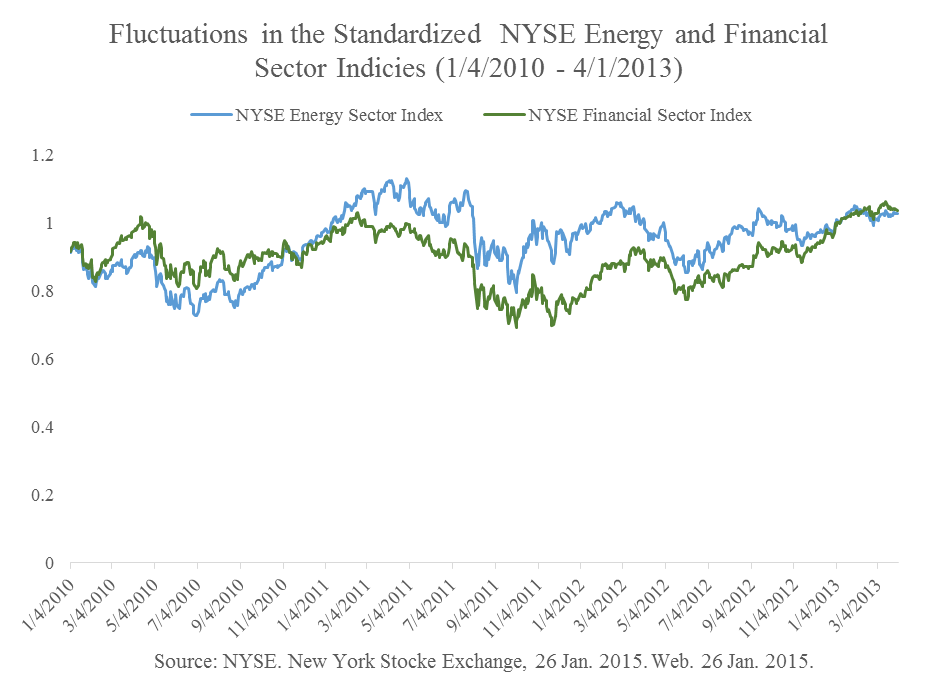

Today, we see a similar ― albeit more contained ― trend of toxic assets permeating the banking sector… instead however, this trend is originating from the energy market:

From a simple aesthetic perspective, it appears that the financial sector is closely following the gains and losses in growth held by the energy sector ― however this is an observation that can also be statistically and scientifically reaffirmed.

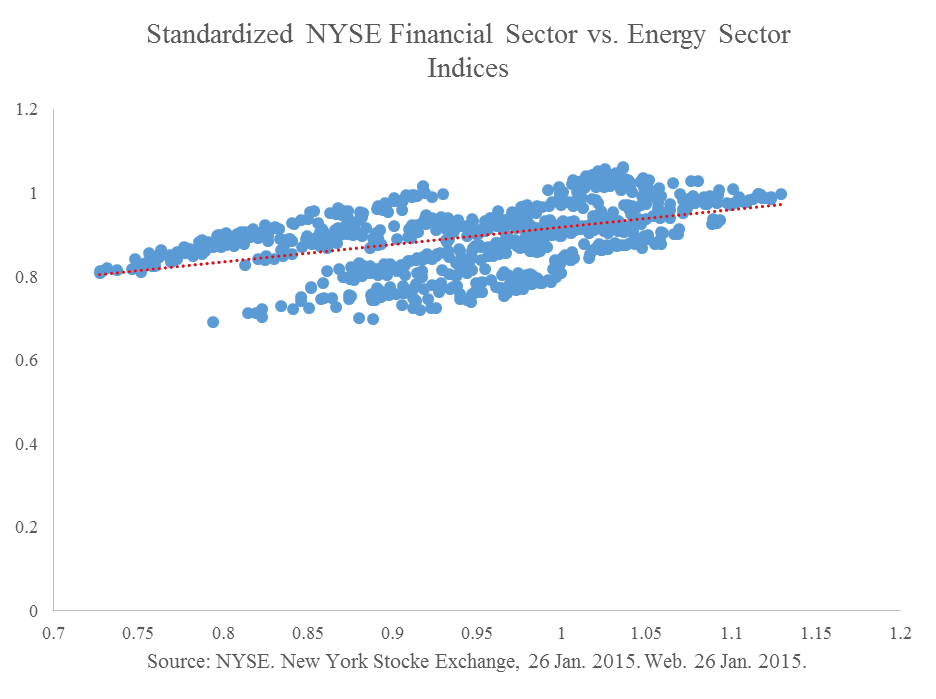

The regression below simply shows a close-knit positive correlation between standardized changes in the two indices. The two sectors expand and contract in close unison, surprisingly with very few instances of outliers.

This financially symbiotic relationship is indicative of a heavy amount of investment by the banking and financial services industry, in the energy industry. Indeed, Seeking Alpha, an online finance and investment research platform proclaims that the Fed’s “relentless interest rate repression,” is credited as the main reason investors turned their back to safer investments in lieu of junk bonds within the energy industry. These specific bonds have been previously been regarded as a source of more stable and higher yielding returns, especially in in the post-recession years. Now however, Main Street investors are playing hot-potato with them, in a manner is oddly similar to the treatment of Mortgage-Backed Securities in 2007-08. Investors are preferring instead to sell them to the smaller influx of Wall Street players such as Goldman Sachs, who tout the precipitously falling value of these bonds as all the more reason to expect higher future returns. But will there be a resurgence in the value of these bonds? At least to their normal level of profitability? Perhaps, but as the Fed begins to hike interest rates, and OPEC continues suppressing prices, it is unlikely that they will ever be viewed to be as attractive as they once were.

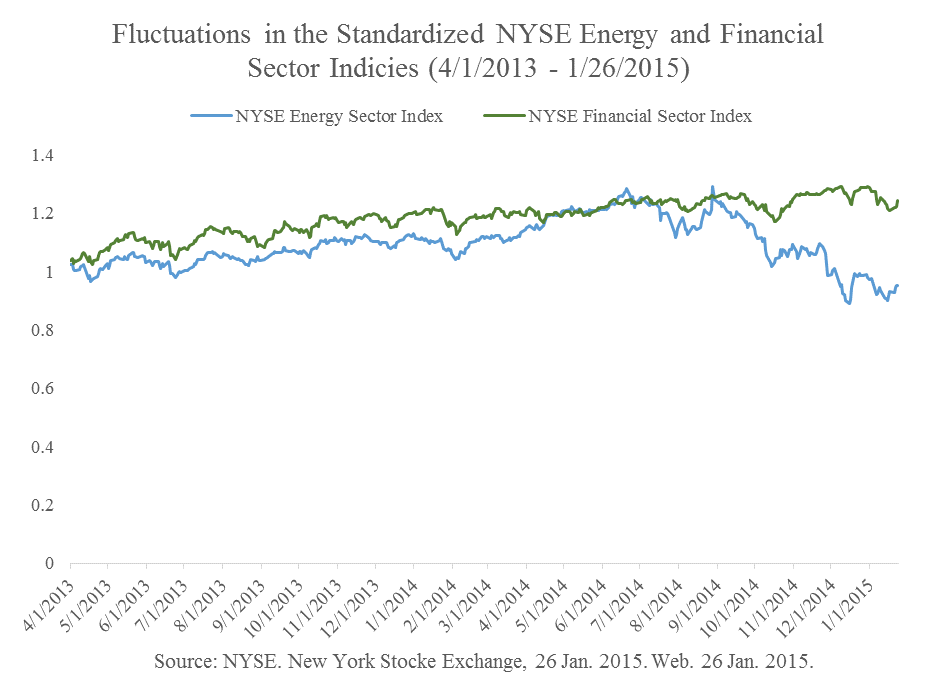

Lastly, it is important to highlight a recent departure from the norm in the financial sector that has been in development since the 3rd quarter of 2014:

Though the two industries still mirror changes within each other, the financial Sector has become increasingly better-off relative to the energy sector. Why? Reasons could include finally hedging investments against volatility in the oil sector, and the renewables sector which has only become less competitive since OPEC’s November announcements… Many of these financial intermediaries however, have not abstained from investments in energy firms and already have outstanding loans that their debtors in the oil business are becoming more and more prone to defaulting on. It is likely that we are simply seeing a lag in the financial sector.

In the same manner that the accumulation of ripples from defaulting on mortgages began the economic tsunami of 2007, the oil industry has the potential to seriously hurt investors abroad and the American financial sector. Sustained or dropping oil prices will only magnify the rate at which public and private assets become the seeds of contagion.